To stick to your project budget, you have to track costs. Project accounting, as with general accounting, is a method by which project managers can manage project finances.

Project accounting is not the same as balancing your checkbook or even seeking the service of a certified public accountant as it’s unique to project management. Let’s look at what a project account is as well as its principles and methods.

What Is Project Accounting?

Project accounting refers to all elements related to financial transactions in a project. This includes everything from project costs, billing and revenue. Project managers and accountants use project accounting when executing financial tasks on projects. Management receives regular reports on its progress and whether or not the project accounting is successful.

The use of project accounting is essential in managing a project budget; project managers use it to stay updated on the project’s direct costs, overhead costs and revenue. Just as a project manager monitors the project’s schedule and scope, they also track these financial transactions to ensure they’re on budget and make necessary adjustments to avoid overspending.

To do this, a project accounting plan must be created during the project planning phase. The plan outlines all costs and schedules how to monitor and track those costs during project execution, including money spent on resources such as the project team, equipment and more.

When creating a project plan, you need project management tools to organize costs related to delivering the product or service on time and within budget. ProjectManager is work and project management software with interactive Gantt charts that help you plan every step of your project on a visual timeline. There are features to plan and manage costs and resources, both human and nonhuman. Set the baseline to track planned costs against actual costs in real time. Get started with ProjectManager today for free.

How Does Project Accounting Work?

Project accounting works by creating a detailed plan of your project costs and managing them throughout project execution to make sure you’re on budget. This is done by monitoring project costs and tracking the variance between the planned and actual costs.

Documentation is required to record the project costs that are incurred throughout the project. As noted, tracking the actual expenses and revenues of the project helps compare them to the costs you have set in your plan, but you’ll also look at future-based costs of contracted delivery schedules and completion dates.

Project accounting includes documenting the date legal agreements are signed with a customer, tracking earned revenues from sales agreements and identifying the costs related to each project phase. In short, project accounting follows the money from the project plan through execution with detailed documentation and adjustments to help you stick to your budget.

Project Accounting Principles

As in any project management method, there are principles to help initiate, plan and establish metrics for accounting in projects, how to execute contracts, avoid scope creep and close out projects. There are eight main project accounting principles that we’ve outlined below.

- Cost principle: When recording the project costs, use the original value instead of the forecasted market value. You want to capture the cost you spent, not the potential cost.

- Matching principle: Revenues and expenses should match the appropriate costs over time. When assigning expenses incurred during project execution, make it the period in the project when the team has incurred the expenses.

- Consolidation principle: To make the overall project cost consistent, group any related project work together. Accomplish this through a systematic process of determining revenue and costs with other parties to consolidate financial activities for the project under one account.

- Full Disclosure principle: You want to record everything of significance in your financial statements to provide transparency into your project finances. This helps with accountability with project stakeholders.

- Prudence principle: This principle requires that you state the amount of revenue and expenses that represents the best estimate of how much revenue or costs might actually occur over the course of the project.

- Liability principle: Make sure to acknowledge all costs related to the future obligations of the project. This can include any contract penalties and liquidation damages associated with the breach of a contract. In other words, you’re liable for these costs if they incur.

- Control principle: You must apply procedures and processes when monitoring the financial activities of the project to make sure you follow regulations. This allows managers to track the actual costs of the project and adjust nonrecurring events to keep to their budget.

- Resource allocation principle: This principle states that resources can be allocated to more than one project. Project managers can allocate the same amount of resources to different projects if there’s a financial benefit and little risk involved rather than continuing to reallocate money over time into projects.

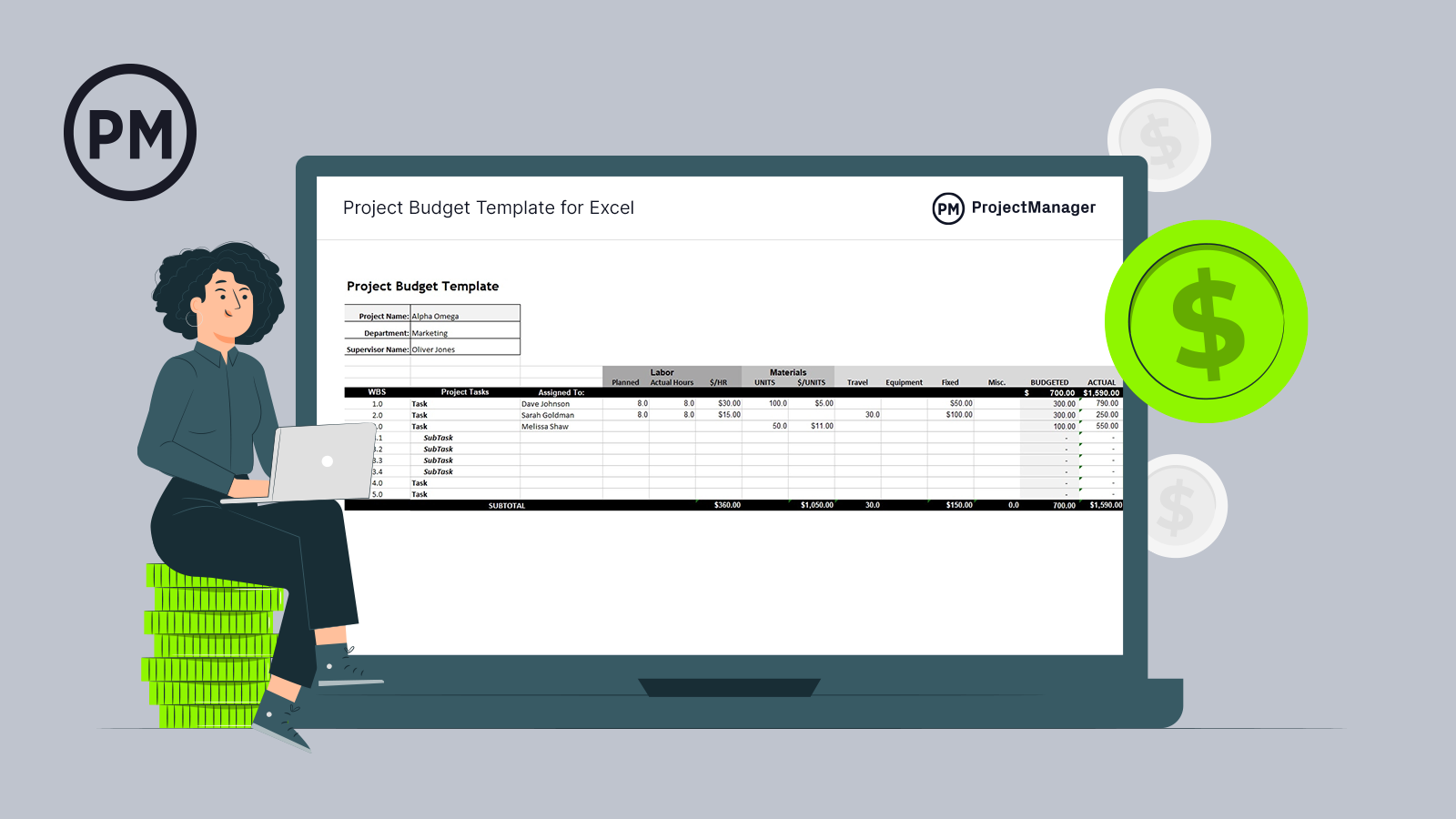

Get your free

Project Budget Template

Use this free Project Budget Template for Excel to manage your projects better.

Project Accounting vs. Financial Accounting

Project accounting and more general financial accounting share many things in common but they’re not the same thing. Yes, they both deal with costs and expenses, but the context and the execution differ enough to make it worth exploring some of those differences.

For starters, there’s a different timetable for project accounting and financial accounting. Project accounting deals with a project, which has a start date and an end date. This means the accounting work ends when the project is completed. Financial accounting works on periods throughout the financial year, which is different across businesses.

The reporting is also different. In project accounting, reporting is based on deliverables. Financial accounting has reports, too, only they look at other aspects of running a business. They’re more concerned with profit and loss, which is not relatable to project accounting.

There are also cost hierarchies that diverge. For example, project accounting cost hierarchies are based on tasks and projects while financial accounting hierarchies are based on departments and cost centers.

Comparative analysis is hard to do in projects but easy in financial accounting. In fact, the levels of understanding are different as well. Stakeholders and sponsors of projects don’t often understand how money is spent on projects, but lenders are clear about financial accounting principles.

Project Accounting Revenue Recognition Methods

Revenue recognition in project accounting is based on when a client should pay, whether upfront, in the middle of the project or when the final deliverable is complete. Revenue recognition only counts revenue once the money has been earned. There are several methods of project accounting revenue recognition, the most common listed below.

Sales Basis

This method recognizes revenue once the sale has been made. That is, at the point of purchase you recognize your revenue. This can be done with cash or credit on the delivery of goods or services. This is commonplace in retail stores but can also apply to project deliverables.

Installment

The installment plan is familiar to anyone who holds a mortgage or has bought large machinery and paid for it over a period of time. There is risk involved as it’s not certain that payment will be delivered regularly. This method means you recognize revenue as it’s delivered as a percentage of the total revenue. This could be over a period of months or even years.

Percentage of Completion

This method is often used with large or long-term projects. It allows a company to recognize revenue by milestones that indicate progress in the project. Contracts for this method are detailed to make it clear when revenue recognition takes place. This allows you to recognize revenue as it comes in instead of waiting until the end of a long project.

Completed Contract

Here, you realize revenue after everything has been delivered and stakeholders or clients are satisfied. This is mostly found with short-term projects or when an extended warranty is involved. It can also end up as a default method when others, such as the percentage of completion method, fail due to lack of clarity.

Cost Recoverability

When you can’t estimate the cost of goods and services in the contract, it’s called cost recoverability. A more conservative approach to revenue recognition only comes to fruition after you’ve recoupled all costs associated with the project.

The Role of the Project Accountant

Project accounting is usually done by the project manager and the project accountant, depending on the size of the project and the organization hosting the project. Project accountants are responsible for monitoring the process of the project, tracking variances and approving expenses.

Project accountants also ensure that project billing is done correctly and delivered to the clients as well as making sure payments are received. They are often in charge of project reporting and maintaining all relevant income and expenditure for the project while also overseeing project records and contracts to ensure they’re followed.

In addition, project accountants review processes for managing accounts and work with auditors. It’s the project accountant’s responsibility to develop financial systems with the IT team in order to be more user-friendly.

Project Accounting Benefits

The importance of project accounting is clear; cost is one-third of the triple constraint and managing those finances is key to delivering a successful project. Knowing how much you’re spending will help you keep to your budget, therefore, understanding the workflow of your costs is crucial to controlling them. Here are some other benefits to project accounting.

- Get insights into costs, bids and scope for new projects

- Improves resource management

- Stay updated on project progress and profitability

- Helps identify issues with projects to respond quickly

- Educates project team on project cost and profitability

- Improves financial management of the organization

- Reduces risk and improves overall project management

How ProjectManager Helps With Project Accounting

The benefits of project accounting are clear, but many cannot be achieved without the proper tools. ProjectManager is work and project management software that captures real-time data for more insightful decision-making. Organize costs and resources and monitor them in real time to better manage your budget and deliver success to your stakeholders.

Streamline Payment and Track Time

Use our timesheets to help you manage your resources. Once a timesheet is submitted, it is locked until an authorized manager can provide approval. It also tracks who is working on what and showcases outstanding tasks and overall workload. You can see who is busy and who has the capacity for more tasks, all of which are important for capacity planning and expense tracking.

Get a High-Level View of Costs and More

While lightweight software tools require manual dashboard configuration, ours is ready to go when you are. It automatically captures and calculates project data that’s displayed in colorful graphs and charts. You can track costs in real time along with five other project metrics. For more in-depth data, use our one-click reports on timesheets, costs and more. All reports can be filtered to show only the information you want to see and easily shared with stakeholders to keep them updated.

ProjectManager lets you make a cost management plan, organize tasks, resources and more. You can set your budget and track it in real time, creating detailed reports to help you stay on schedule and within budget. All your project accounting needs are built into our myriad of features which help you plan, monitor and report on every aspect of your project. Take account of your project with the only project management tool you’ll need.

ProjectManager is award-winning work and project management software for hybrid teams. Our collaborative platform helps you work better together, no matter where, when or what department. There’s a single source of truth that keeps everyone on the same page. Join the tens of thousands of teams using our tool to deliver success at organizations as varied as NASA, Siemens and Nestle. Get started with ProjectManager today for free.